Q-1: What is e-invoicing?

Ans: Electronic invoicing or e-Invoicing is a process of generating invoices, under which invoices created by one software can be accessed by other software, removing the requirement for any new data entry or errors. In less difficult words, it is an invoice generated utilizing a standard format, where the electronic information of the invoice can be shared to other people, consequently ensuring compatibility of information.

Q-2: Is e-invoicing mandatory?

Ans: E-invoicing is compulsory for all businesses with an annual turnover of Rs. 100 crore or more with effect from 1st January 2021. Earlier it was applicable on businesses with turnover exceeding the limit of Rs. 500 crore.

However e-invoicing is not applicable to the below-written categories irrespective of the business turnover, as stated in CBIC notification no. 13/2020- central tax:

- An insurer or a banking company or a financial institution, including an NBFC

- A Goods Transport Agency (GTA)

- A registered person supplying passenger transportation services

- A registered person supplying services by way of admission to the exhibition of cinematographic films in multiplex services

- An SEZ unit (excluded via CBIC Notification No. 61/2020 – Central Tax)

Q-3: How e-invoicing is beneficial?

Ans: Below are the main benefits of e-Invoicing:

- One-time reporting of B2B invoices at the time of generation, which reduces the time of reporting in multiple formats.

- The majority of the information in structure GSTR-1 can be saved prepared for documenting while at the same time utilizing e-invoicing format.

- E-way bills can likewise be created effectively utilizing e-Invoice data.

- There is no need to reconcile the books and GST returns filed.

- Invoices can be tracked in real-time by the supplier, with the quicker accessibility of information tax credit. It also reduces the tax credit verification issues.

- Better administration and automation of the tax filing process.

- Less fraudulent invoices.

Q-4: Does the e-invoice schema apply to RCM transactions?

Ans: Yes, the e-invoice schema is applicable to reverse charge mechanism (RCM) transaction.

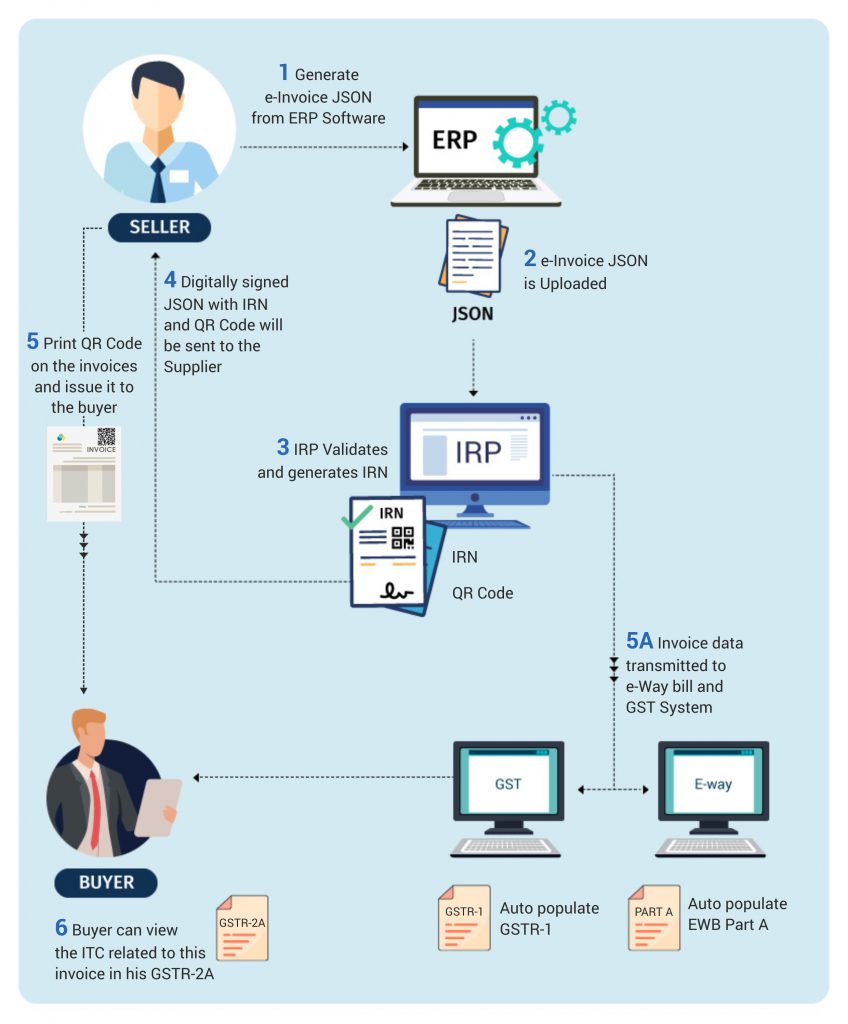

Q-1: What is the process of e-invoicing?

Ans: There are not many changes; businesses can continue to generate their invoices from their existing software just as before. To ensure a level of standardization only a standard format, the schema will be used to generate the e-invoices. The generation of these systematic invoices will be done by the taxpayer. While generating the invoices, he/she has to report it to the GST Invoice Registration Portal (IRP). Then the portal will generate a unique invoice reference number & adds the digital signature along with the QR code on to the e-invoice. The QR code contains all the required details of the e-invoice. After all this process the e-invoice will be returned to the taxpayer by the portal. IRP will also send a copy of the signed invoice to the registered email-id of the seller.

Q-2 How the process will look like?

Ans: The process of an e-Invoice involved two major parts-

- In the first part the business/supplier and the Invoice Registration Portal (IRP) is involved.

- In the second part the IRP and the GST/E-Way Bill Systems are involved.

Q-3: How to create an e-invoice?

Ans: You can create an e-invoice with the following four methods:

- Offline tool

- Using GST Suvidha Provider

- Through Direct Integration

- Via API integration with sister concern GSTIN

- Using E-way Bill API credentials

Offline method-

- To generate IRN for bulk using offline tool, you can simply download the offline tool from the portal: https://einvoice1.gst.gov.in/

- Then enter the details of the invoice & check it, validate it

- Generate the JSON file & upload it on to the portal

For all other methods the taxpayer has to first register the APIs by logging in to the portal. Then he/she has to use the API credentials to connect & generate IRN & e-way bill.

{kind=link}