There may be various reasons for the cancellation of the e-invoices and some of them are as follows:

- Cancellation of the order by a buyer

- Incorrect entry of any goods mentioned in the bill

- The duplicate entry of the same bill etc.

To cancel an e-Invoice on the IRP, a taxpayer needs to follow the given steps:

Step 1: Firstly, Log in to the e-Invoice portal, thereafter in the left section of the portal select the option ‘E-invoice’.

Now in ‘E-invoice’ Tab select ‘Cancel’.

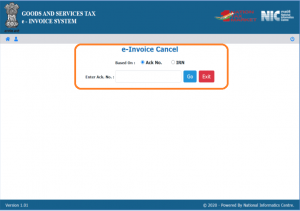

Step 2:

E-invoice cancel window will appear

- Mention the basis of cancellation of the e-invoice i.e. ‘Ack No or IRN’

- Select ‘Ack No’

- Now in ‘Enter ACK no’ mention you acknowledgement no of your invoice

- Click on ‘Go’

Thereafter the portal will display that the invoice has been successfully cancelled. And the cancelled e-Invoice will be displayed with a ‘Cancelled’ watermark.

{kind=link}